Navigating the EU Corporate Sustainability Reporting Directive (CSRD)

Navigating the EU Corporate Sustainability Reporting Directive (CSRD)

Understand what the CSRD is, who does it apply to and how to become compliant

In this week's edition of our sustainability newsletter, we explore the European Union's (EU) significant advancement toward a more sustainable future with the Corporate Sustainability Reporting Directive (CSRD). This new regulation marks a critical leap in our shared path towards enhanced transparency and responsibility in environmental, social, and governance (ESG). By examining the complexities of the CSRD, it becomes evident that its goals extend beyond mere compliance, aiming instead to cultivate a culture of sustainable development and resilience within EU businesses and beyond.

The Essence of the CSRD

The CSRD is a regulatory framework introduced by the European Union to enhance the scope and quality of sustainability reporting among companies. It extends the obligations of corporate reporting beyond traditional financial metrics to include detailed ESG aspects.

The CSRD's required reporting disclosures are outlined in the EU Sustainability Reporting Standards (ESRS). ESRS was developed by the European Financial Reporting Advisory Group (EFRAG), and adopted and published by the European Commission on July 31, 2023.

Who Needs to Comply?

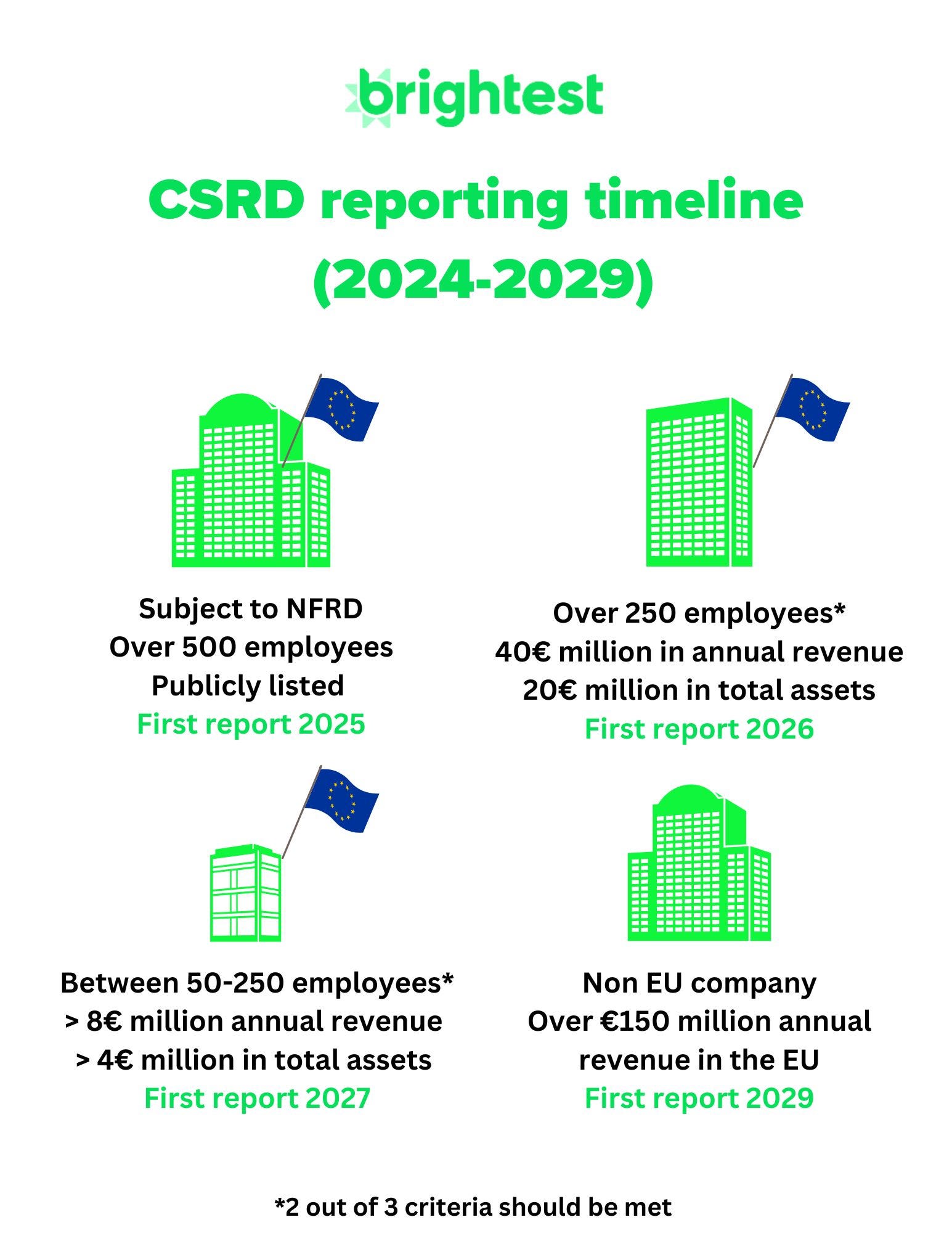

Starting from January 1, 2024, the CSRD applies to large companies and public-interest entities in the EU, affecting over 50,000 businesses.

The CSRD is rolled out in phases with:

Large companies (over 500 employees and publicly listed) previously covered by the NFRD (Non-financial Reporting Directive) who start reporting under the CSRD from 2024, with the first reports due in 2025.

Large companies (with over 250 employees, and/or more than 40€ million in annual revenue, and/or 20€ million in total assets)* will need to comply starting in 2025, with their initial reports expected in 2026.

SMEs (small and medium-sized businesses) in the EU or outside the EU but listed on the stock exchange will begin reporting from 2026, with their first reports due in 2027. These SMEs may have the option to delay reporting until 2028.

Non-EU companies with a cumulative group turnover in the EU greater than €150 million are required to report from 2029 for financial years starting on or after January 1, 2028.

*2 out of these 3 criteria should be met

What Does Compliance Entail?

Compliance with the CSRD requires companies to prepare and submit a detailed report on their sustainability practices and impacts. This encompasses a wide range of disclosures with a total of 12 ESRS (European Sustainability Reporting Standards) including:

ESRS 2: General disclosures

ESRS Environmental E1: Climate change

ESRS Environmental E2: Pollution

ESRS Environmental E3: Water and marine resources

ESRS Environmental E4: Biodiversity and ecosystems

ESRS Environmental E5: Resource use and circular economy

ESRS Social S1: Own workforce

ESRS Social S2: Workers in the value chain

ESRS Social S3: Affected communities

ESRS Social S4: Consumers and end-users

ESRS Governance G1: Business conduct

In order to identify which standard to report on companies should start their reporting journey with a double materiality assessment which will allow to assess which topics are material (that is relevant) for your business.

Preparing for the CSRD

Complying with the CSRD can be daunting, so let’s break it down in some steps you can take to get started with CSRD reporting:

Internal Alignment: The first step is to understand when you need to report and make sure your organization and especially your board is aware of the regulation.

Conduct your Double Materiality: While performing a double materiality assessment is mandatory, this step will allow you to identify which topics you should be reporting on and what data you will need to collect.

Move to Implementation and Action: Craft a detailed timeline to draft your report, start collecting data and keep an eye on your progress.

Conclude with Reporting and Assurance: Compile your findings into a report, make sure to audit your report for limited assurance, make your findings public, and aim to continuously improve your performance.

Key Points to Remember

Here are some points you should keep in mind when starting your journey to becoming CSRD compliant:

Make sure to create a CSRD task force: while sustainability teams are often very lean, it is key to make sure that the right counterparts are involved. Some key departments in your organization to include in the task force are Finance, Marketing, HR, Operations, and IT.

You may exclude topics which are immaterial: the CSRD contains 82 disclosures and a total of 1,144 data points to report on. It is however not mandatory to report on all data points as they may not all be relevant to your organization. Performing a double materiality assessment will enable you to identify the relevant data points for your organization.

Embrace CSRD as an opportunity: complying with the CSRD is of course not an easy task, it is however an opportunity to showcase your sustainability commitment and lead the way towards a greener future.

Conclusion: A Catalyst for Change

The introduction of the CSRD marks a pivotal moment in the European Union's environmental and social governance agenda. By requiring detailed sustainability reporting, the directive not only aims to foster transparency and accountability but also to encourage companies to integrate sustainable practices into their core operations. As we move forward, the CSRD is expected to play a crucial role in driving positive change, inspiring businesses to not only meet regulatory requirements but to innovate and lead in sustainability. Let's embrace this opportunity to redefine the future of business, creating a more sustainable, resilient, and equitable world for generations to come.

This Week in Sustainability is a weekly email from Brightest (and friends) about sustainability and climate strategy. If you’ve enjoyed this piece, please consider forwarding it to a friend or teammate. If you’re reading it for the first time, we hope you enjoyed it enough to consider subscribing. If we can be helpful to you or your organization’s sustainability journey, please be in touch.